Managing Cash has

never been easier

Clip offers a nationwide network of self-service locations for convenient business deposits, digital transaction tracking and reporting, and fast change delivery services.

The choiсe is yours

With Clip, you’re in control. Whether you deposit nearby ATM, daily or weekly, one thing remains constant. Freedom.

No long-term contracts, no minimums, no commitments. We don’t lock you in. You decide when and where to deposit or order change, and you only pay for the solutions we provide.

monthly

savings

saved

weekly

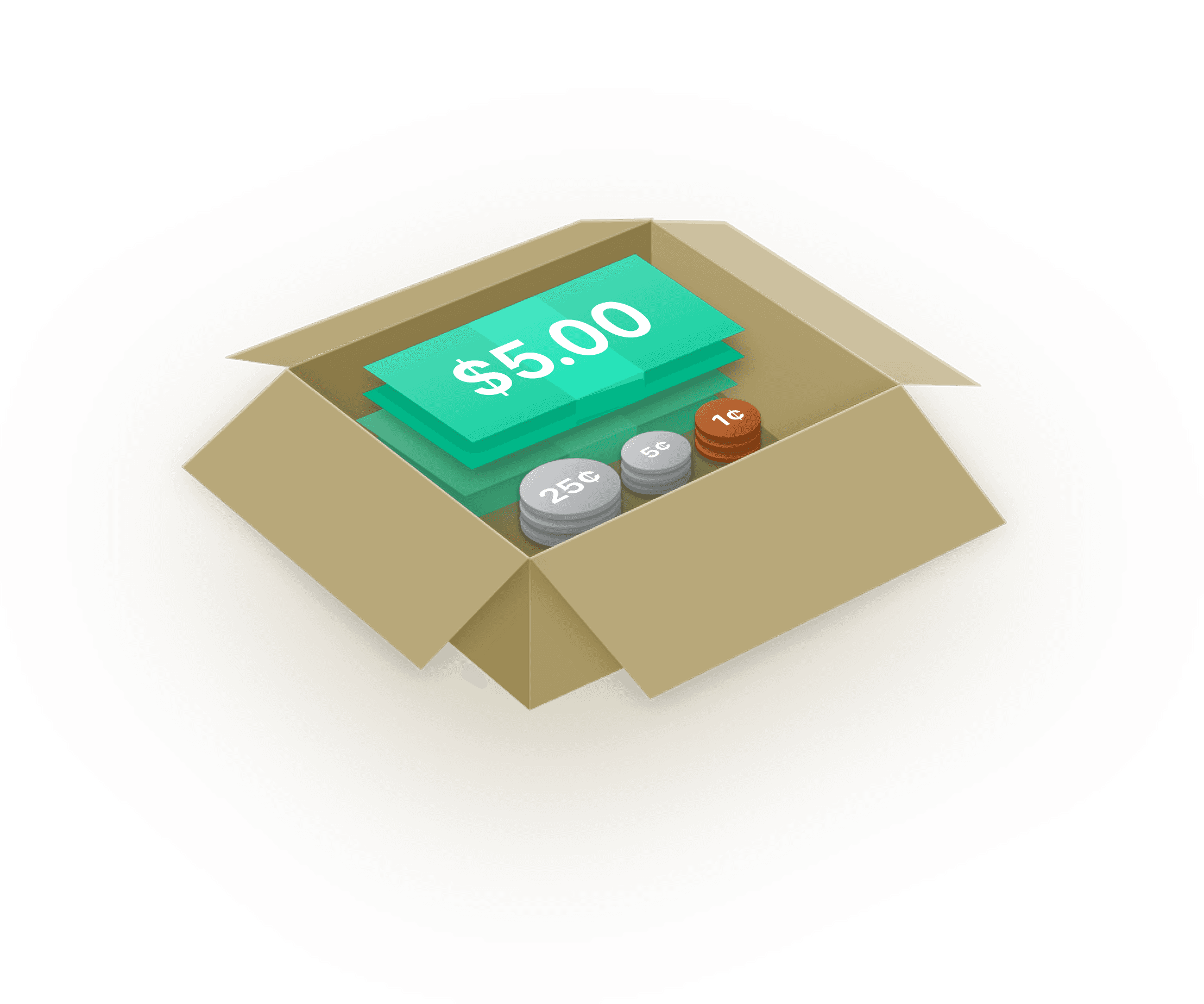

Whether you operate a single store or manage a chain of a thousand, every business that partners with us reaps the same remarkable benefits: substantial monthly savings per store and the invaluable return of countless employee hours.

We treat our customers like partners

Our journey began with a simple mission: make depositing cash easier. But we didn’t stop there. By listening to business owners like you, we’ve pioneered products and solutions that are redefining the cash management industry with innovations never seen before. Frustrated with the antiquated options available to you in the market? It’s time for Clip.

The Cashboard

The Clip Cashboard brings everything together, from store-level cash data to employees to bank accounts, in one unified platform.

Filter. Track. Report. Our digital cash transformation platform is powered by amazing software designed for speed and ease of use. Create multiple deposit types, order change, or manage employees and stores — the Cashboard makes it all so easy. Learn More about the Clip Platform, or contact sales today.